The financial side of a UK visa application isn’t about hitting a specific number. It’s about convincing a caseworker that your stated purpose and finances match, that your money is genuinely yours, and that you can fund the trip without working illegally or relying on public funds. This guide breaks down how caseworkers actually assess bank statements, the 28-day principle, and the scenarios that cause refusals.

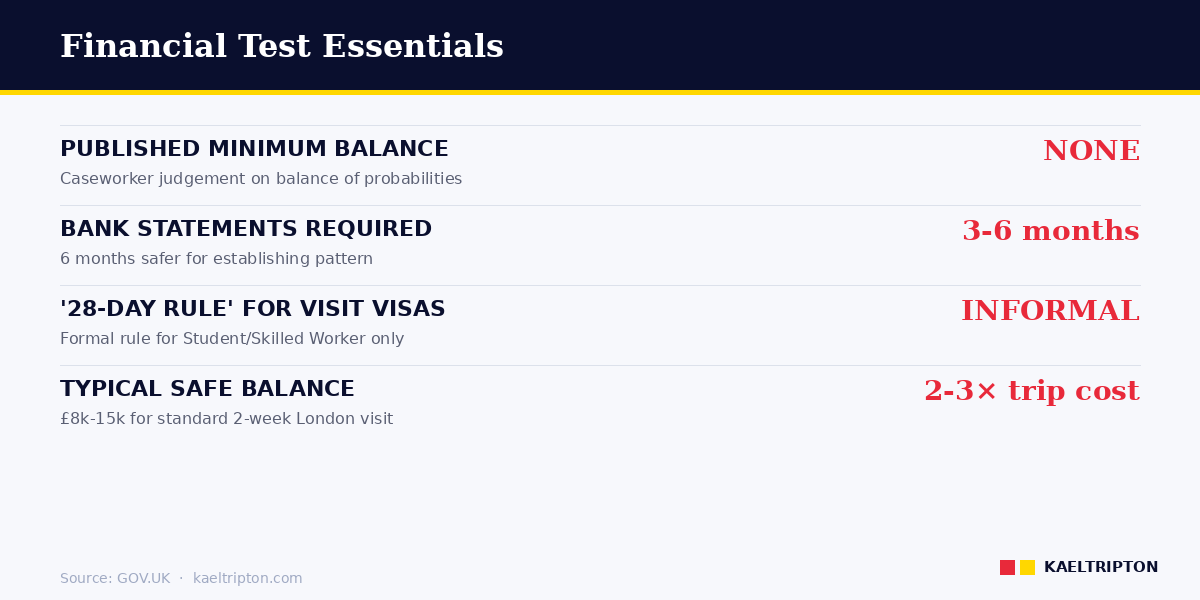

No published minimum balance for UK visit visas — caseworkers assess on the balance of probabilities whether funds are credible, genuine, and sufficient for the trip. Rough working standard: 2-3x expected trip cost, with 6 months of consistent bank statements showing income and expenditure pattern. Sudden large deposits without source-of-funds evidence is the single most common cause of refusal for financially capable applicants. |

The core financial test

UK visa applicants must demonstrate that they have sufficient funds to cover all reasonable costs of their visit without working or accessing public funds. This is paragraph V 4.5 of Appendix V of the Immigration Rules. The rule doesn’t specify a number — it specifies a standard. Caseworkers decide on the balance of probabilities whether your finances are credible given your stated purpose, length of stay, and activities.

There is no published “minimum balance” for the Standard Visitor visa. The Home Office Visit: Caseworker Guidance (25 February 2026) explicitly rejects the idea of a numeric threshold. Instead, caseworkers assess whether the amount shown is consistent with the applicant’s stated circumstances, the trip costs, and the financial pattern before application.

What caseworkers actually look at

Per paragraph V 4.5 and the published Visit caseworker guidance, three questions drive the financial assessment:

- Can the applicant cover all costs of the trip? Flights, accommodation, daily expenses, and any special activities stated. The caseworker compares balances against trip costs that reasonable research would suggest.

- Are the funds genuinely available to the applicant? Not borrowed briefly to show the statement, not transferred in from friends to inflate the balance, not tied to a business the applicant doesn’t legally control.

- Is the financial pattern consistent with the applicant’s stated income and employment? A stated monthly salary of £500 doesn’t explain an account balance of £30,000 without additional context.

A caseworker looking at your bank statements is not auditing. They’re checking whether the picture holds together.

The 28-day principle

Immigration lawyers often mention a “28-day rule” for UK visa bank statements. This isn’t a published Home Office rule for visit visas — it comes from the longer-stay visa categories (Student, Skilled Worker) where funds must be in the account for at least 28 consecutive days before application to count toward the maintenance requirement.

For visit visas, there is no strict 28-day rule, but the underlying principle applies: caseworkers are sceptical of funds that appeared recently. A balance that materialised three weeks before application is flagged, not because of a specific 28-day rule but because of paragraph V 4.5’s “genuinely available” test.

Practical working standard: have your funds in place for at least 6 months of continuous bank statements. This removes any ambiguity about source and genuineness.

Bank statements — what to provide

Caseworkers expect to see:

- 3 to 6 months of recent bank statements in the applicant’s name. 6 months is safer than 3 for establishing a pattern.

- Official bank-issued PDFs or stamped paper statements. Not screenshots, not screenshots compiled into a PDF, not third-party aggregator exports. The document must be traceable to the bank.

- Statements covering the account the applicant uses for primary income and expenses. Not a secondary account with an idle balance.

- Evidence of regular income credits consistent with stated employment or self-employment.

- Rent, EMI, utilities and other recurring debits consistent with stated lifestyle.

What to avoid:

- Statements with large unexplained deposits close to application date.

- Accounts cycled — repeated transfers between your own accounts close to application.

- Third-party deposits you cannot explain (for example, an amount from a relative with no documented relationship).

- Any signs of coaching — round-number deposits, identical amounts from multiple sources, timed to show a specific balance.

Source-of-funds documentation

If your bank statements show any significant deposit that a caseworker might question, pre-emptively document its source. A single line of evidence is usually enough:

| Deposit source | Evidence to include |

|---|---|

| Salary bonus | Employer letter confirming the bonus amount and date |

| Property sale | Sale deed; bank receipt of proceeds |

| Business income | GST returns, Income Tax Returns, business bank statements showing the transfer to personal |

| Inheritance | Will or probate document; death certificate of the deceased |

| Gift from family | Relationship evidence (birth certificate), giver’s bank statement showing the outward transfer, gift declaration letter |

| Loan (personal or family) | Loan agreement, lender’s bank statement — but note that borrowed funds may not count as “genuinely available” |

| Investment maturity | Investment statement showing the redemption |

Borrowed funds are treated cautiously. If your balance shows a recent loan from a family member with the explicit purpose of funding the trip, the caseworker may assess whether you have independent means without that loan. Loans aren’t banned but they don’t always count toward “genuinely available” funds.

Trip cost estimation

Caseworkers have reasonable expectations of what a UK trip costs. For a 2-week Standard Visitor visit staying in moderate hotels in London, the caseworker assumes something in the range of:

- Flights: £400-800 return depending on origin.

- Accommodation: £100-200 per night = £1,400-2,800 for 14 nights.

- Food and local travel: £50-100 per day = £700-1,400.

- Activities, shopping, miscellaneous: £500-1,000.

Total expected range: £3,000-6,000 for a standard 2-week London trip. An applicant showing a £500 bank balance cannot fund this without borrowing. An applicant with £200,000 in the account for a 2-week Standard Visitor trip raises different questions — why is so much liquid cash needed, and is the money genuinely theirs.

A reasonable bank balance for a standard 2-week London trip demonstrates somewhere in the range of 2-3x the expected trip cost — roughly £8,000-15,000 shown — with a consistent pattern of income and expenses. You don’t need to be rich; you need to be credible.

Sponsor letters — when someone else is paying

If a UK-based or overseas sponsor is covering your costs, their documentation becomes part of your financial case:

- Relationship evidence — how you know the sponsor. Family relationships via birth or marriage certificates. Employer sponsorship via employment contract and letterhead.

- Sponsor’s bank statements — 3-6 months showing their ability to cover the trip costs without depleting their savings.

- Sponsor’s immigration status if UK-based: passport photo page, share code from gov.uk/view-prove-immigration-status, or BRP if held.

- Sponsor’s employment letter confirming their income and job stability.

- Sponsor’s own accommodation evidence if you’re staying with them — utility bill, tenancy agreement, council tax statement.

- Sponsor letter explicitly confirming their relationship to you, the trip costs they will cover, and their commitment.

Caseworkers verify the sponsor’s legitimacy. A student-visa holder sponsoring three relatives from a shared room raises questions. A British citizen homeowner sponsoring their parent for two weeks does not.

Scenario — the financially capable but badly documented applicant

Consider a realistic case. A chartered accountant in Bengaluru earns ₹1.5 lakh (£1,400) per month. She saves steadily and has built up ₹12 lakh (£11,200) in her savings account over 3 years. She applies for a UK Standard Visitor visa for a 2-week London trip in August 2026.

Her bank statements cover the last 3 months and show the ₹12 lakh balance with a couple of large recent deposits: ₹2 lakh in March 2026 and ₹3 lakh in April 2026. These were her annual bonus and her tax refund, respectively — both legitimate, but her application doesn’t explain them.

The caseworker sees the deposits, sees no explanation, and refuses under V 4.5 for “insufficient evidence of genuinely available funds.”

Reapplication: she provides 6 months of statements (extending the window), her employer letter explicitly mentioning the bonus amount and date, and her Income Tax Return showing the refund. Same balance; context added; approved.

Teaching point: financial capability without documented context is not enough. A competent caseworker can’t tell the difference between genuine savings and coached balances without source evidence. Provide the context proactively.

Scenario — the young applicant with modest funds

A second case. A graduate student in Dhaka (finished Master’s, working first job) earns approximately £400 per month. His balance over 3 months sits at £1,200 — small savings. His father, a senior government official, will fund his 10-day UK visit to attend a cousin’s wedding.

His application includes his own bank statements (showing his modest but consistent pattern), his father’s sponsor letter stating the relationship, the father’s bank statements (£45,000 balance from long government employment), his father’s employment confirmation, and the wedding invitation card. Approved on the strength of the combined financial case and the documented sponsor relationship.

Teaching point: an applicant with modest personal funds succeeds if the sponsor case is solid. Building the sponsor’s evidence — not just a letter but bank statements and employment proof — is what transforms a borderline case into an approval.

Self-employed applicants

Self-employed applicants need evidence that self-employment actually generates the income stated:

- Business registration documents (GST registration, incorporation certificate, sole trader registration).

- Income Tax Returns for the last 2-3 assessment years with acknowledgement receipts.

- Business bank statements (separate from personal) for 6 months, showing transaction activity.

- Evidence of specific contracts, invoices, or client relationships if the business is service-based.

- Personal bank statements showing transfers from business to personal where relevant.

Freelancers without formal incorporation can use personal bank statements alone if the income is transparently from self-employment, plus tax returns.

Retirees and applicants without employment

Retired applicants use pension credits as their income pattern. A UK state pension, an Indian PPF or EPF maturity, a Singapore CPF payout — any documented retirement income works as evidence of “genuinely available” funds, provided the statements show credits consistent with the pension scheme’s rules.

Applicants without current employment or retirement income rely on savings and sponsor documentation. The caseworker judges whether the savings are genuine (6 months of statements, no recent unexplained deposits) and whether the stated reason for the trip is consistent (visiting family, medical treatment, short business visit).

Red flags that cause refusal

The single most common refusal-triggering patterns in financial documentation:

- Large deposit in the weeks before application with no source-of-funds evidence.

- Rapid cycling — repeated transfers in and out of the account to show a balance.

- Third-party deposits from people not documented as family or sponsors.

- Bank statements that don’t match the stated income from the employer letter.

- Screenshots or third-party exports instead of bank-issued documents.

- Non-English statements without certified translation.

- Funds sitting in a business account when the applicant is not the legal owner of the business.

Currency, translation and format requirements

Bank statements in currencies other than GBP are accepted at face value — caseworkers convert mentally using current exchange rates. No pre-conversion required. What matters is that the balance in local currency covers the trip when converted.

Statements in languages other than English or Welsh require certified translation. A certified translator stamps and signs each page confirming the translation is accurate. Self-translation is not accepted, nor is Google Translate output, nor is a friend’s translation without certification. Certified translators are available in most major cities; expect to pay £20-50 per page.

Format matters too. Bank statements should be full-page PDFs from the bank’s online portal, ideally downloaded directly rather than exported through third-party apps. Scanned paper statements work if the scan is high-quality and shows the bank’s letterhead, all transaction details, and the statement period clearly. Screenshots of mobile banking apps are the weakest form — they can look edited and caseworkers treat them with scepticism.

Related guides

- UK Visitor Visa 2026

- UK Visa from India 2026

- UK Visa Refusal Reasons 2026

- UK Visa Application Status Check 2026

Disclaimer

This guide reflects Home Office Visit caseworker guidance and Appendix V of the Immigration Rules as published on GOV.UK as of April 2026. There is no published minimum balance for visit visas; caseworkers assess on the balance of probabilities. For complex financial histories, sponsor arrangements, or previous refusals under V 4.5, consult an OISC-regulated immigration adviser or UK immigration solicitor. This article is not financial or legal advice.

Frequently asked questions

How much money do I need in my bank account for a UK visa?

No published minimum. Caseworkers assess whether your balance is consistent with your stated trip costs, employment income, and financial pattern. For a standard 2-week London Standard Visitor visit, a balance roughly 2-3x expected trip costs (£8,000-15,000) with a documented source is typically enough. £500 balance with £4,000 trip costs fails; £200,000 balance with no income pattern raises different questions.

What is the 28-day rule for UK visas?

The 28-day rule is a formal requirement for Student, Skilled Worker and Family visas — funds must be in the account for 28 consecutive days before application. For Standard Visitor visas, no strict 28-day rule exists, but the underlying principle applies: caseworkers are sceptical of recently-appeared balances. Have your funds in place for at least 6 months of continuous statements for visit visas.

Do I need to submit 3 months or 6 months of bank statements?

GOV.UK asks for at least 3 months. In practice, 6 months is safer. It establishes a clearer pattern and makes any recent deposits harder to question. For applicants with sudden deposits, large balances, or non-obvious income sources, 6 months is effectively necessary.

Can someone else pay for my UK visa trip?

Yes. A sponsor — family member, employer, or organisational host — can fund your trip. You must provide the sponsor’s bank statements (3-6 months), relationship evidence (birth/marriage certificates or employment contract), sponsor’s immigration status if UK-based, and a sponsor letter explicitly committing to cover specific costs. The sponsor’s financial capacity is assessed alongside your own.

Why was my UK visa refused for “insufficient funds” when I had enough money?

Usually the issue isn’t the amount — it’s that the caseworker judged the funds weren’t “genuinely available” to you. Common causes: a recent large deposit without source-of-funds evidence, a balance inconsistent with your stated income, sponsor funds but weak sponsor documentation, or borrowed money that doesn’t count as your own. Context and source evidence, not total balance, is what passes the test.

Can I use statements from a joint account for a UK visa?

Yes, if the account is in your name (jointly with spouse, parent, or business partner). Caseworkers accept joint accounts where you have independent access and are a named holder. For spouse-joint accounts, include both partners’ names and evidence of the relationship. Pure third-party accounts — your parent’s account where you’re not a holder — don’t count toward your personal finances but can support a sponsor relationship.

What evidence do I need for a large deposit?

Depends on the source: employer letter for a bonus; sale deed for property proceeds; Income Tax Return for a tax refund; probate document for inheritance; business accounts for self-employed earnings. A single line of credible evidence for each significant deposit usually suffices. Don’t hide large deposits — proactive documentation is what removes the caseworker’s concern.

Sources

- Home Office — Visit: Caseworker Guidance (25 February 2026, published on GOV.UK)

- GOV.UK — Immigration Rules: Appendix V Visitor

- GOV.UK — Visit the UK as a Standard Visitor

- GOV.UK — View and prove your immigration status

- GOV.UK — Immigration Rules Part 9: Grounds for Refusal