Company car tax is charged through Benefit-in-Kind (BiK) — HMRC's mechanism for taxing non-cash employment benefits. When an employer provides a car for personal (non-business) use, the tax treats the private benefit as additional income. For 2026-27, EV BiK rises from 2% to 3% of the car's P11D value. Plug-in hybrids pay BiK bands of 5-14% depending on electric-only range. Standard petrol and diesel cars pay 25-37% depending on CO2 emissions. Your actual tax is BiK % × P11D value × your marginal income tax rate (20%, 40%, 45% or 47% Scottish top rate). Fuel benefit adds another layer if the employer also pays for private fuel. This guide covers 2026-27 rates with realistic worked examples.

| ★ EDITOR'S VERDICT EV company cars via salary sacrifice save £200+/month for higher-rate taxpayers. |

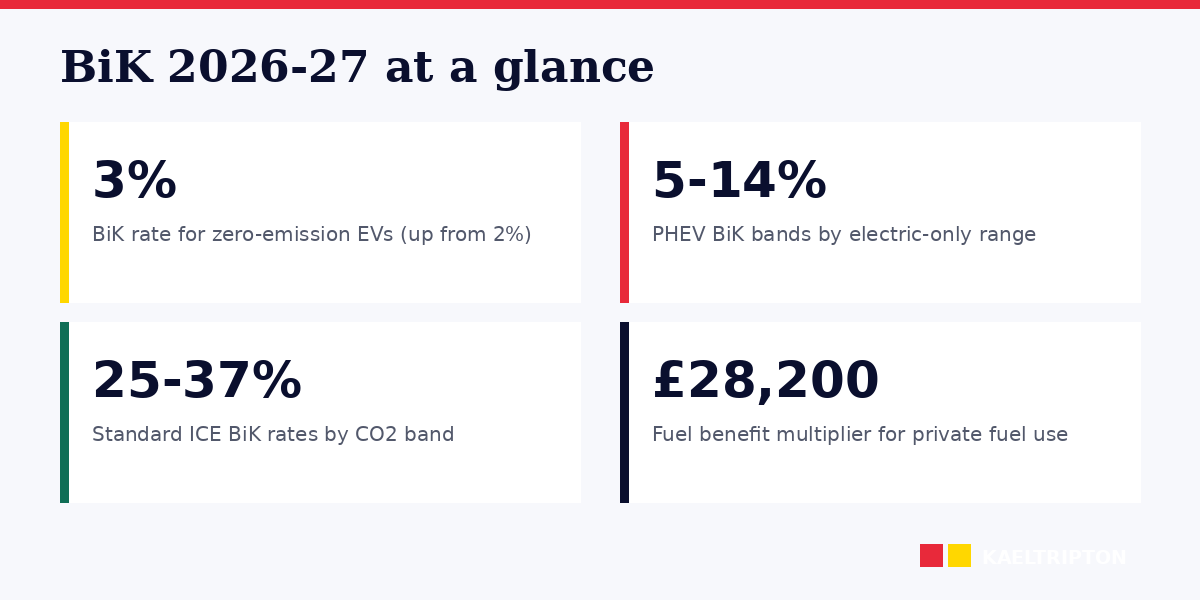

2026-27 Benefit-in-Kind rates: EV at 3% (up from 2%), PHEVs 5-14% by electric range, ICE cars 25-37% by CO2. A £40,000 EV costs around £40/month in company car tax. The equivalent 37% BiK ICE car costs £493/month plus another £348 if fuel benefit applies — a £800/month gap. Salary sacrifice EV schemes save higher-rate taxpayers £150-£250/month via tax and NI efficiency versus personal lease. Fuel benefit charge is £28,200 × BiK% for 2026-27 — employees increasingly pay their own fuel to avoid this. |

How Benefit-in-Kind works

BiK is calculated in three steps:

- Identify the P11D value — the manufacturer's list price when new, including delivery, VAT, and optional extras. Discounts from the dealer do NOT reduce the P11D value.

- Apply the BiK percentage — determined by the car's CO2 emissions, fuel type, and for hybrids the electric-only range

- Multiply by your marginal income tax rate — 20%, 40%, 45% (England and Wales), or higher in Scotland (up to 47%)

The result is your annual company car tax liability, typically paid monthly via PAYE from your salary.

Worked example: £40,000 P11D company car with 25% BiK band, 40% marginal tax rate:

- Taxable benefit: £40,000 × 25% = £10,000

- Tax payable: £10,000 × 40% = £4,000/year

- Monthly cost via PAYE: £333

2026-27 BiK rates by fuel type

Zero-emission electric vehicles

EVs benefit from the lowest BiK rate in the system:

- 2025-26: 2%

- 2026-27: 3% (increase confirmed)

- 2027-28 onwards: scheduled gradual increases — confirmed incrementally each year

The 3% rate means a £50,000 EV generates £1,500 in BiK for the year. At 40% tax, the employee pays £600/year in company car tax — a genuinely low figure compared to ICE equivalents.

Plug-in hybrids by electric-only range

Plug-in hybrids (PHEVs) have BiK rates 2026-27 that depend on the vehicle's all-electric range measured under WLTP. The longer the electric range, the lower the BiK band:

| Electric-only range (miles) | 2026-27 BiK rate |

|---|---|

| 130+ miles | 5% |

| 70-129 miles | 8% |

| 40-69 miles | 11% |

| 30-39 miles | 14% |

| Under 30 miles | based on CO2 emissions (see below) |

Short-range PHEVs (under 30 miles electric) lose the preferential band treatment and fall into the main CO2 bands along with standard hybrids.

Petrol and diesel cars

Standard ICE cars use CO2 bands. 2026-27 rates start at 25% and rise 1% per 5 g/km CO2 above 75 g/km:

- 0-75 g/km: 25%

- 76-80: 26%

- 81-85: 27%

- 86-90: 28%

- 91-95: 29%

- 96-100: 30%

- 101-105: 31%

- 106-110: 32%

- 111-115: 33%

- 116-120: 34%

- 121-125: 35%

- 126-130: 36%

- 131+: 37% (top rate)

Diesel cars pay an additional 4% surcharge unless they meet the Real Driving Emissions Step 2 (RDE2) standard. Most diesels registered from January 2021 meet RDE2. Diesels registered 2018-2020 vary. Earlier diesels generally don't meet RDE2.

The 37% top rate has been reached for many medium-CO2 cars. Practical effect: a £40,000 petrol car with 140 g/km CO2 pays BiK on £40,000 × 37% = £14,800 taxable benefit, which at 40% tax equals £5,920/year.

Hybrid cars (non-plug-in)

Standard hybrids (HEVs, like Toyota Prius, Honda Civic Hybrid) use the same CO2 bands as petrol and diesel. Their relatively low CO2 (typically 80-110 g/km) puts them in bands 26-32%. No special PHEV benefits because they can't run on electric only.

Fuel benefit: the hidden additional cost

If your employer pays for your private fuel as well as company fuel, an additional fuel benefit applies. For 2026-27:

- Fuel benefit charge: £28,200 × BiK % for that vehicle (up from £27,800 in 2025-26)

- Example: £40,000 company car with 25% BiK, fuel benefit = £28,200 × 25% = £7,050 taxable benefit

- At 40% tax: £2,820/year in fuel benefit tax

Fuel benefit is punitive for higher-CO2 cars. Many employees now pay their own fuel and claim business miles back at HMRC Approved Mileage Rates (45p/mile for first 10,000 business miles, 25p thereafter) to avoid the fuel benefit charge entirely.

For EVs, charging at work doesn't count as a taxable benefit — the 3% BiK covers everything including workplace charging, which is a significant perk for EV company car drivers.

Salary sacrifice: the EV advantage

Salary sacrifice arrangements let employees exchange salary for benefits. For EV company cars, this structure is particularly tax-efficient:

- Employee agrees to reduce gross salary by the monthly cost of the EV lease

- Reduced salary means reduced income tax and NI for the employee

- Employer passes the lease cost through

- Employee pays BiK at 3% (2026-27) on the EV's P11D value

- Net result: the employee pays for the EV using tax-efficient pre-tax income

For a £40,000 EV via salary sacrifice at £450/month gross:

- Pre-tax cost: £450/month

- Income tax saving at 40%: £180/month

- NI saving at 2%: £9/month

- BiK cost: £40,000 × 3% × 40% / 12 = £40/month

- Net cost to employee: £450 - £180 - £9 + £40 = £301/month

Equivalent personal lease: typically £400-£500/month for the same vehicle. The salary sacrifice structure saves £100-£200/month for higher-rate taxpayers.

Major providers: Octopus Electric Vehicles, Loveelectric, Tusker, Pink Salary Exchange. Most schemes include insurance, maintenance, tyres, and breakdown in the monthly figure.

A real 2026 scenario: company car comparison

A 42-year-old marketing manager earning £75,000 (40% marginal tax rate) is choosing between three company car options, all with £40,000 P11D value:

Option A — petrol 2.0L SUV, 155 g/km CO2, BiK 37%

- Taxable BiK: £40,000 × 37% = £14,800

- Annual tax: £14,800 × 40% = £5,920 (£493/month)

- + fuel benefit: £28,200 × 37% × 40% = £4,174 (£348/month)

- Total: £841/month if fuel benefit applies

Option B — plug-in hybrid, 42 miles electric, BiK 11%

- Taxable BiK: £40,000 × 11% = £4,400

- Annual tax: £4,400 × 40% = £1,760 (£147/month)

- + fuel benefit if applicable: £28,200 × 11% × 40% = £1,240 (£103/month)

- Total: £250/month with fuel benefit, or £147 without

Option C — fully electric, BiK 3%

- Taxable BiK: £40,000 × 3% = £1,200

- Annual tax: £1,200 × 40% = £480 (£40/month)

- No fuel benefit charge — workplace charging included

- Total: £40/month

The difference between Option A and Option C is £800/month — approximately £9,600/year in take-home pay. For higher earners, the EV is dramatically tax-efficient. Most UK company car fleets have shifted heavily toward EVs since 2020 for this reason.

The P11D declaration cycle

BiK is reported annually via Form P11D:

- Employer obligation: submit P11D to HMRC by 6 July each year for the previous tax year

- Copy to employee: provided by the same deadline

- PAYE tax collection: HMRC adjusts the employee's tax code to collect BiK through PAYE over the following tax year

- P46(Car): submitted separately when a company car is first provided, changed, or withdrawn

Errors in BiK calculation sometimes arise from incorrect P11D value (missing optional extras, wrong list price), incorrect CO2 banding, or incorrect electric range for PHEVs. Review your P11D annually and query discrepancies with HR or payroll.

Frequently asked questions

Is company car tax really better than taking a salary increase?

Depends heavily on the vehicle. EVs via salary sacrifice or provided as company cars are substantially cheaper than equivalent personal purchase for higher-rate taxpayers. Petrol/diesel cars often cost MORE in BiK than you'd save with cash-instead salary — the crossover is around 25-30% BiK rate for most scenarios.

How is P11D value calculated?

Manufacturer's list price when new plus delivery, VAT, and all optional extras. Dealer discounts, cashback offers, or negotiated price reductions do NOT reduce P11D value. The P11D figure is fixed at the point the employer takes the vehicle and doesn't change year-on-year as the car depreciates.

Do I pay BiK on the work vehicle I only use for commuting?

If you use the vehicle for any personal purpose beyond commuting (including stopping at the shops on the way home), BiK applies. Pure workplace use with no personal element (car kept at work, only driven between sites) can avoid BiK — but the rules are strict and verified by HMRC.

What happens if my company car is provided via salary sacrifice?

Same BiK rules apply — the tax treats it as a company car regardless of the funding mechanism. The tax efficiency comes from the combined income-tax-and-NI saving on the sacrificed salary, minus the BiK cost. EVs benefit hugely; ICE cars generally don't.

Can I avoid company car tax by paying myself mileage?

Yes, if the vehicle is truly yours (personal lease or purchase) and you claim business mileage at HMRC Approved Mileage Rates (45p/mile first 10,000, 25p thereafter). This avoids company car BiK entirely but removes employer-funded vehicle costs. Works well for heavy personal use; less cost-effective for high-mileage drivers.

Does the 3% EV BiK rate apply to my private EV?

No — it only applies to company-provided EVs. Your privately-owned EV has no BiK. The 3% rate is specifically for vehicles an employer makes available for personal use.

What about vans and pickup trucks?

Commercial vehicles have separate BiK rules — typically a flat £3,960 van benefit charge plus £757 van fuel charge (2026-27 figures) regardless of vehicle value. Much simpler than car BiK but can be substantial for higher-rate taxpayers using pickup trucks as company vehicles. Some pickups with heavy payloads qualify as "light commercial" rather than "car" for BiK purposes — HMRC has specific guidance on this.

Sources

- HMRC, Expenses and benefits: company cars and fuel — gov.uk/expenses-and-benefits-company-cars

- HMRC, BiK rates for 2026-27 published in Finance Act provisions

- GOV.UK, Company car and car fuel calculator

- HMRC, Approved Mileage Allowance Payments (AMAP) rates

- HMRC, Form P11D and P11D(b) guidance

- Finance Act 2023 and subsequent Finance Acts — EV BiK rate schedule

- HMRC, Salary sacrifice: optional remuneration arrangements