Setting up UK car tax by direct debit is straightforward. Cancelling it, changing the payment card, or dealing with a failed payment is where it gets less obvious. This guide walks through the 5% monthly surcharge that makes DD more expensive than people realise, how DVLA handles failures, and the exact routes to cancel or change.

DVLA vehicle tax direct debit carries a 5% surcharge on monthly and six-monthly payments. Annual direct debit has no surcharge and is the cheapest way to pay. Cancel by bank, via gov.uk/vehicle-tax, by phone, or by triggering a sale/SORN event. Two consecutive failed collections (common cause: expired card) lead to DVLA cancelling the DD and treating the vehicle as untaxed — the £80 LLP follows automatically. |

How DVLA direct debit actually works

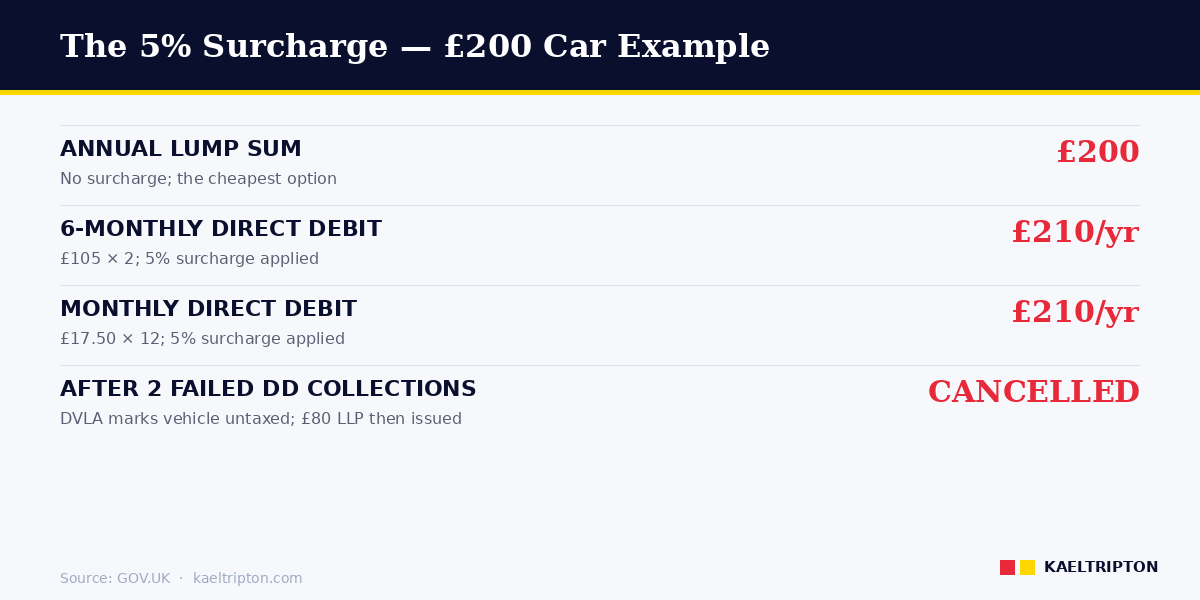

DVLA accepts vehicle tax by direct debit in three payment frequencies: monthly, six-monthly, or annually. Monthly and six-monthly carry a 5% surcharge; annual direct debit has no surcharge. The surcharge is applied to the equivalent annual rate, so monthly direct debit on a £200 car works out to £17.50 per month, totalling £210 per year. Six-monthly works out to £105 per half, totalling £210 per year.

You set up direct debit at gov.uk/vehicle-tax during the normal tax-renewal journey, or at a Post Office counter. You cannot set up direct debit by phone — the automated phone service does not offer it.

Direct debit continues automatically. DVLA does not contact you before each collection. Once set up, payments continue year after year unless you cancel, the card/account changes, or a trigger event occurs (sale, SORN, scrap, export).

The 5% surcharge — what it actually costs

| Annual VED rate | Annual DD | 6-monthly DD | Monthly DD | Monthly total (12 months) |

|---|---|---|---|---|

| £20 | £20 | £10.50 × 2 = £21 | £1.75 | £21 |

| £200 | £200 | £105 × 2 = £210 | £17.50 | £210 |

| £640 | £640 | £336 × 2 = £672 | £56 | £672 |

The £640 example is the total for a car attracting the expensive car supplement (£200 standard + £440 supplement). Paying monthly on such a car costs £32 more per year than annual.

If cashflow isn’t the issue, annual direct debit is the cheapest way. If you need to spread cost across the year, monthly at 5% surcharge is the option — still cheaper than a credit card charged monthly with interest.

Setting up direct debit — the specific process

Setting up at gov.uk/vehicle-tax:

- Enter your V11 reminder reference, V5C reference, or V5C/2 new-keeper reference.

- Confirm vehicle details.

- Choose payment frequency (annually, six-monthly, monthly).

- Enter your UK bank account details (sort code, account number, name on account). The account must be in your own name and authorised for direct debit.

- Complete the Direct Debit Guarantee acceptance.

- Receive confirmation by email.

The first payment is collected 5 to 7 working days after setup. Subsequent payments are collected on the same day each month (or the 6-month/annual anniversary).

Cancelling direct debit — four routes

Direct debit cancellations happen in four ways:

- Through your bank. Call your bank, or cancel via online banking. This is a standard direct debit cancellation under the Direct Debit Guarantee. Your bank must cancel on request, instantly.

- Via DVLA online. At gov.uk/vehicle-tax, you can end the current tax and direct debit. Requires your V5C or V11 reference.

- By phone to DVLA. Call 0300 123 4321. Automated service accepts cancellation requests.

- Automatically at a trigger event. If you sell the vehicle, scrap it, export it or declare SORN, DVLA automatically cancels the direct debit. You don’t need to do anything separately.

If you cancel through your bank without notifying DVLA, DVLA sees the payment fail and treats the vehicle as untaxed after a specific failure pattern (see the section below). Bank cancellation alone does not tell DVLA you no longer want to tax the vehicle; you need to SORN it or re-tax in a different payment method if you want to keep using it legally.

Changing payment details

DVLA does not offer an online “update payment details” journey separate from cancelling and restarting. To change the bank account or debit card linked to your direct debit:

- Cancel the current direct debit (via bank, DVLA online, or phone).

- Set up a new direct debit using the new bank account, at gov.uk/vehicle-tax or a Post Office.

The gap between cancellation and new setup is where vehicles become technically untaxed. If you cancel on the 20th and don’t re-set-up until the 25th, those five days are an enforcement risk. In practice DVLA’s system takes a few days to mark the vehicle as untaxed, so short admin gaps don’t usually trigger an LLP — but timing it carefully is wise.

What happens when a direct debit payment fails

This is the failure mode that catches most drivers out. DVLA’s enforcement policy sets out how failed payments are handled.

On the first failed collection (insufficient funds, card expired, account closed), DVLA attempts a second collection a few working days later. If the second collection also fails, DVLA cancels the direct debit instruction and treats the vehicle as untaxed from that date.

DVLA does not send a warning SMS or email when the first payment fails. Some banks do (your bank’s overdraft alerts, for example), but that’s bank-side, not DVLA-side. DVLA’s first communication is the automatic £80 late licensing penalty after the vehicle has been flagged as untaxed.

Common failure triggers:

- Expired payment card. Banks increasingly tie direct debits to card accounts rather than bank accounts; when the card expires, the DD bounces.

- Changed bank account without updating DVLA. The old account closes, DVLA tries to collect, fails.

- Insufficient funds on collection day.

- Business account restrictions. Some corporate-account direct debits are blocked.

Scenario — the expired card

Consider a realistic case. A copywriter in Bristol sets up monthly direct debit at £17.50 in April 2025. Her bank card expires in May 2026. Her bank automatically issues a new card number for physical payments but does not update the card-linked direct debit identifier.

On 14 May 2026 DVLA tries to collect the May payment. Fails. DVLA retries on 19 May. Fails again. On 20 May DVLA cancels the direct debit and marks the vehicle as untaxed.

On 24 May, ANPR on the M32 flags her car as untaxed. An £80 LLP arrives. She pays £40 within 33 days, re-sets up direct debit with the new card details, and moves on — £40 plus one month of back-VED spent on what was effectively a banking paperwork issue.

Teaching point: check your vehicle tax status at gov.uk/check-vehicle-tax if your bank card is about to expire, or after any bank account change. Don’t wait for the LLP to arrive.

Switching to annual payment

If you want to stop paying the 5% surcharge, you can switch from monthly to annual payment at any time. The process:

- Cancel the current monthly direct debit (via bank, DVLA online, or phone).

- Wait for the current month’s payment to clear (if already taken).

- Re-tax the vehicle at gov.uk/vehicle-tax choosing annual payment in a lump sum by card.

The lump-sum payment covers the rest of the current tax year. At the next renewal date, you can set up annual direct debit (no surcharge) or simply pay by card again.

Direct debit is not an obligation. You can change the payment method at each annual renewal without any DVLA consequence, provided the vehicle is taxed continuously.

The direct debit guarantee

All UK direct debits, including DVLA VED direct debits, are covered by the Direct Debit Guarantee — a standard agreed by banks and enforced by industry body Bacs. Key protections:

- If any error is made by DVLA or your bank, you’re entitled to an immediate refund from your bank of the full amount.

- You can cancel a direct debit at any time by contacting your bank.

- DVLA must give you at least 10 working days’ notice of changes to collection amount or date.

In practice, DVLA VED direct debits are low-risk because amounts are fixed (tied to annual VED rates) and collection dates don’t change mid-year. But if a DVLA error does occur — duplicate collection, wrong amount — your bank refunds you under the guarantee immediately, and DVLA then reclaims from you if appropriate.

Related guides

- How to Tax Your Car Online UK 2026

- How to Renew Vehicle Tax UK 2026

- Untaxed Vehicle Penalty UK 2026

- UK Car Tax Refund How to Claim 2026

Disclaimer

Rates and processes in this guide reflect DVLA direct debit rules published on GOV.UK as of April 2026. The 5% surcharge is set by legislation and can change. Always verify at gov.uk/vehicle-tax before setting up. This article is not financial advice.

Frequently asked questions

Is UK car tax direct debit more expensive than paying annually?

Yes, for monthly and six-monthly payments. Both carry a 5% surcharge on the annual rate. A £200 annual rate costs £210 if paid monthly (£17.50 × 12) or six-monthly (£105 × 2). Annual direct debit has no surcharge. The cheapest option is paying the annual rate in a single direct debit or card payment.

How do I cancel my UK car tax direct debit?

Four routes: call your bank (or cancel via online banking), cancel online at gov.uk/vehicle-tax using your V5C or V11 reference, call DVLA on 0300 123 4321, or trigger an event (sell, SORN, scrap, export) that DVLA records — which cancels the DD automatically. Cancellation via your bank alone doesn’t stop the vehicle being considered taxed by DVLA; DVLA will see the payment fail and eventually treat the vehicle as untaxed.

What happens if my DVLA direct debit fails?

DVLA retries the collection a few working days later. If that also fails, DVLA cancels the direct debit and treats the vehicle as untaxed from that date. The first notice you typically receive is the automatic £80 late licensing penalty after ANPR detection or a DVLA register scan. DVLA does not send an advance warning text or email when a payment fails.

Can I change the bank account linked to my DVLA direct debit?

Not directly. DVLA doesn’t offer an “update payment details” option. You cancel the current direct debit and set up a new one at gov.uk/vehicle-tax using the new account. Do this promptly — the gap between cancellation and new setup is when the vehicle is technically untaxed, though short admin gaps rarely trigger an LLP.

Does setting up direct debit start paying immediately?

First payment is collected 5 to 7 working days after setup. Before that first collection, DVLA treats the vehicle as taxed from the date of setup. Subsequent payments are collected on the same day each month (or at 6-month/annual anniversary) for the frequency you chose.

Can I pay DVLA direct debit from a joint account?

Yes, but the account must be authorised for direct debit and the account holder (one of the named holders) must have consented. DVLA doesn’t check who is the registered keeper against the account — that’s between you and the account holder. For family-owned cars, using a shared account is common and works fine.

What if I set up direct debit but then sell the car?

DVLA automatically cancels the direct debit when the change of keeper is processed. The unused full months of VED that you paid are refunded to the direct debit account within six weeks. You don’t need to cancel the DD separately; the sale notification handles both tax cancellation and refund.

Sources

- GOV.UK — Tax your vehicle (including direct debit setup)

- GOV.UK — Vehicle tax Direct Debit payments

- GOV.UK — DVLA Vehicle Enforcement Policy

- GOV.UK — Check if a vehicle is taxed

- Bacs — Direct Debit Guarantee (standard industry agreement)