UK car tax refunds are automatic. You don’t fill in a form, don’t apply, don’t chase. But timing and the full-month rule mean thousands of drivers lose money they thought they’d claimed. This guide covers what triggers a refund, the full-month rule that catches sellers out, and the specific DVLA process that determines when and how you get paid.

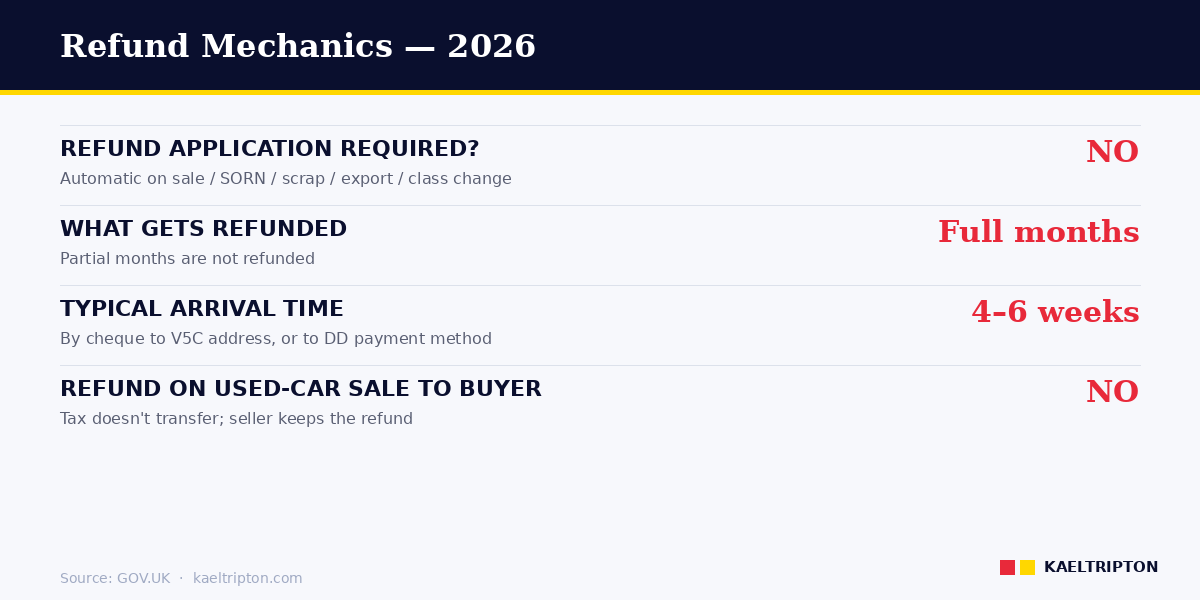

UK car tax refunds are automatic at DVLA. No form, no application. Trigger events: sale, SORN, scrap, permanent export, or tax-class change. Only full remaining months refund — partial months are lost. Cheque arrives at V5C address within 4–6 weeks, or back to the direct debit account. Tax does not transfer to used-car buyers: seller keeps the refund, buyer must tax anew. |

The refund rule, in one sentence

When a UK-registered vehicle is sold, scrapped, permanently exported, declared SORN, or becomes exempt from vehicle tax, DVLA automatically refunds the registered keeper for any full remaining months of the current tax period. Refunds arrive within six weeks by cheque to the registered keeper’s address or back to the direct debit source. There is no refund form; no application required.

“Full months” is the single most misunderstood part. A sale processed on 2 June does not give you a refund starting from 2 June. It gives you a refund for July onwards. The first three days of June are lost — they were part of the month the sale happened in, which counts as used.

The five trigger events

DVLA generates an automatic refund when one of these events is recorded on your vehicle’s record:

| Event | What triggers the refund | Typical timing |

|---|---|---|

| Sold the vehicle | Notify DVLA via gov.uk/sold-bought-vehicle or V5C section 2 | Refund within 6 weeks of DVLA processing |

| Scrapped the vehicle | Authorised Treatment Facility notifies DVLA of destruction | Refund within 6 weeks |

| Permanently exported | Notify DVLA with V5C/4 export section | Refund within 6 weeks |

| Declared SORN | Online, phone or post declaration to DVLA | Refund within 6 weeks |

| Vehicle tax class changed (e.g. to Disabled or Historic) | Post Office processes the class change | Refund within 6 weeks |

What does not trigger a refund: transferring the vehicle between family members without a DVLA change-of-keeper notification, garaging a vehicle that isn’t formally SORN’d, or simply not driving the vehicle. DVLA’s records are the only trigger. If you don’t tell DVLA, no refund happens.

The full-month rule — worked example

This is where most of the confusion lives. DVLA refunds only whole calendar months remaining from the month after the trigger event. Partial months are not refunded.

Worked example. You’re paying £200 annually, with tax running 1 April 2026 to 31 March 2027. The daily rate works out to about £0.55 per day. You sell the vehicle on 12 June 2026. DVLA processes the change on 14 June.

- The month of June is classed as used. No refund for June.

- Months refunded: July, August, September, October, November, December, January, February, March — 9 full months.

- Refund calculation: £200 ÷ 12 × 9 = £150.

- This arrives by cheque within 6 weeks, or back to your direct debit payment method.

Teaching point: time a deliberate sale or SORN to the end of a month if possible, not the start. Selling on 30 June gives you the same refund as selling on 1 July. Selling on 2 July loses you 28 days of July.

How the refund arrives

If you paid annually by card or in a lump sum at a Post Office, DVLA sends a cheque to the registered keeper’s address shown on DVLA records. The cheque is in the keeper’s name. If you’ve moved and not updated your V5C address, the cheque goes to the old address. This is a persistent pain point — DVLA does not chase unclaimed cheques, and after three months they’re stale-dated.

If you paid by monthly direct debit, DVLA cancels the direct debit at the trigger event and credits any overpaid amount back to the payment method. No cheque. Appears in the bank account within the refund window.

If you paid via the six-monthly payment option, the refund works the same way — full remaining months only, calculated as a proportion of what you paid in that six-month period.

Scenario — the seller’s refund trap

Consider a realistic case. A sales manager in Nottingham owns a 2021 Kia Sportage, VED £200 per year, paid in a lump sum in April 2026. In July 2026 she’s promoted and transferred to a company-car scheme. She sells the Sportage privately on 20 July.

At the sale, she completes V5C section 2 (new-style V5C) with the buyer’s details. She hands the V5C/2 green slip to the buyer. A week later she remembers to go online to gov.uk/sold-bought-vehicle and formally notify DVLA of the sale. DVLA processes the notification on 28 July.

Refund calculation: July is a used month (sale happened in July). August through March is 8 full months. £200 ÷ 12 × 8 = £133. Cheque arrives early September.

Teaching point: delayed notification to DVLA costs money. If the sale happened on 20 July but DVLA wasn’t notified until 15 August, DVLA would record August as the trigger month and the refund would be July+7 other months = actually no, DVLA uses the date the sale is processed. The date the sale happened doesn’t override the processing date. Notify on the day of sale.

Direct debit refunds — the subtlety

Monthly direct debit VED carries a 5% surcharge on the annual rate. If your car’s annual rate is £200, direct debit works out to £17.50 per month (£210 per year). If you trigger a refund event halfway through the year, DVLA’s refund calculation uses the effective annual rate you paid, not the standard annual rate.

Worked example: you set up direct debit at £17.50 per month in April 2026. In September you declare SORN. DVLA has collected 6 months (April through September) = £105 paid. The October through March portion (6 months unused, all full months) generates the refund: £17.50 × 6 = £105 refunded to the bank account. The direct debit is automatically cancelled at the next cycle.

In practice, if you set up direct debit and cancel after a few months, you don’t actually save compared to just paying the annual rate — the surcharge absorbs most of the benefit. Where monthly DD wins is cashflow (spreading £210 over 12 months vs £200 up front).

When the refund doesn’t arrive — what to do

Most refunds arrive within 4 to 6 weeks of the trigger event. If nothing has arrived after 8 weeks:

- Check the trigger was actually recorded. Go to gov.uk/check-vehicle-tax and enter the registration. Confirm the tax status shows “not taxed” or the class has changed to what you expected (SORN, Disabled, Historic).

- If you sold the vehicle, confirm DVLA received the notification. The buyer’s new V5C arriving at their address is a good proxy. If they haven’t had it after 4 weeks, DVLA likely didn’t receive your notification.

- Check your V5C address matches your current postal address. DVLA sends cheques to the address on the V5C, not to any separate address you may have given.

- Call DVLA on 0300 790 6802 (Monday to Friday 8am-7pm, Saturday 8am-2pm). Have your V5C reference ready.

DVLA does not proactively re-issue cheques that bounce back. Unclaimed refunds linger in the DVLA finance system — staff can re-issue on request, but you have to make the call.

Edge case — stolen or written-off vehicles

If your vehicle is stolen, the refund process is the same as for scrapping — notify DVLA of the loss with any crime reference number and V5C, and refund follows. If your insurer writes the vehicle off as a total loss (Category A, B, S or N write-off), the insurer usually notifies DVLA as part of the claim process, which triggers the refund to you.

For stolen vehicles that are subsequently recovered, your insurance company typically handles the tax situation depending on who now owns the vehicle. If you retain the recovered vehicle, you’ll need to re-tax it. If the insurer paid out and now owns the vehicle, they handle any further tax.

Edge case — refund on death of keeper

If the registered keeper dies, the vehicle’s tax situation depends on what happens to the vehicle. If the executor transfers it to a beneficiary, that’s a change of keeper triggering the refund for unused months, payable to the deceased’s estate. If the vehicle is sold or scrapped from the estate, same refund trigger. The refund cheque is made out to the registered keeper’s name; executors deposit via the estate’s bank account under probate rules.

Refund and new-keeper confusion

Common buyer complaint: “I bought a taxed car and didn’t get the remaining tax.” Correct — that’s the 2014 rule working as intended. The seller’s tax refunds to the seller; the buyer must tax the vehicle anew. This design prevents abuse (selling a car with tax, then the buyer reselling with the same tax). Each keeper taxes in their own name; each gets their own refund when they in turn stop being the keeper.

The corollary: when you sell a car, factor the remaining months’ VED into your asking price as value you’re giving up, not as something the buyer is receiving. Private sellers often don’t — they let the buyer assume they’re getting “taxed” when in fact the seller will pocket the refund.

Related guides

- SORN Statutory Off Road Notification UK 2026

- Car Tax When Buying a Used Car UK 2026

- How to Tax Your Car Online UK 2026

- How to Check If a Car Is Taxed UK 2026

Disclaimer

Processes described in this guide reflect DVLA procedures published on GOV.UK as of April 2026. Refund mechanics can change without notice if DVLA updates its payment systems. Always verify current practice at gov.uk/vehicle-tax-refund. This article is not financial or legal advice.

Frequently asked questions

How do I claim a UK car tax refund?

You don’t claim — it’s automatic. When you sell, scrap, export, SORN, or change tax class on a vehicle, DVLA automatically refunds any full remaining months of the current tax period. The refund arrives within six weeks by cheque to the registered keeper, or back to the direct debit source. No form needed.

How long does a DVLA tax refund take?

Typically four to six weeks from the date DVLA records the trigger event. Cheques arrive in the post to the address on your V5C. Direct debit refunds appear in the original bank account. If nothing has arrived after eight weeks, call DVLA on 0300 790 6802 to chase.

Do I get a refund if I sell the car mid-month?

Only for complete months after the sale month. If you sell on 12 June, June counts as used and you’re refunded from July onwards. Selling on 30 June or 1 July gets the same refund — there’s no incentive to drag the sale past month-end. Selling on 2 July loses you 28 days of July’s VED.

How is the refund calculated?

Annual rate divided by 12, multiplied by the number of full remaining months. For a £200 annual rate with 8 full months remaining: £200 ÷ 12 × 8 = £133. For direct debit payers, DVLA uses your effective monthly rate (which includes the 5% surcharge). Partial months are not refunded.

Do I get the remaining tax when I buy a used car?

No. Since October 2014, tax does not transfer to the buyer. The seller receives the refund automatically; you must tax the vehicle anew in your own name before driving. Factor this into negotiations: a car with six months of tax “remaining” is not more valuable to a private buyer — that tax refunds to the seller, not you.

What if my DVLA refund cheque gets lost?

Call DVLA on 0300 790 6802 with your V5C reference and trigger event details. DVLA can check whether the cheque was cashed and re-issue if not. Cheques go stale after three months (UK banking standard) so call promptly. Update your V5C address at gov.uk/change-address to prevent future cheques going to an old address.

Can I get a refund for tax I paid years ago that should have been exempt?

No. DVLA refunds only unused full months in the current licence period. If you were eligible for the disability exemption or historic vehicle status earlier but didn’t apply, prior years’ VED is not refundable. Apply for exemption classes as soon as eligibility begins — each delayed month is money you can’t recover.

Sources

- GOV.UK — Cancel your vehicle tax and get a refund

- GOV.UK — Tell DVLA you’ve sold, transferred or bought a vehicle

- GOV.UK — When you need to make a SORN

- GOV.UK — Tax your vehicle

- GOV.UK — Check if a vehicle is taxed

- GOV.UK — DVLA Vehicle Enforcement Policy