INSURANCE GUIDE

Home Emergency Cover UK

What home emergency insurance covers for boiler breakdown, plumbing, and electrical failures.

TL;DR

- Home emergency cover pays for emergency call-outs when a failure makes your home unsafe or uninhabitable.

- It covers labour and parts for the emergency repair up to a per-event limit.

- Boiler breakdown is the most common home emergency claim - but age and condition conditions apply.

- Home emergency cover is not the same as a boiler service plan - the latter includes annual servicing.

What Home Emergency Cover Includes

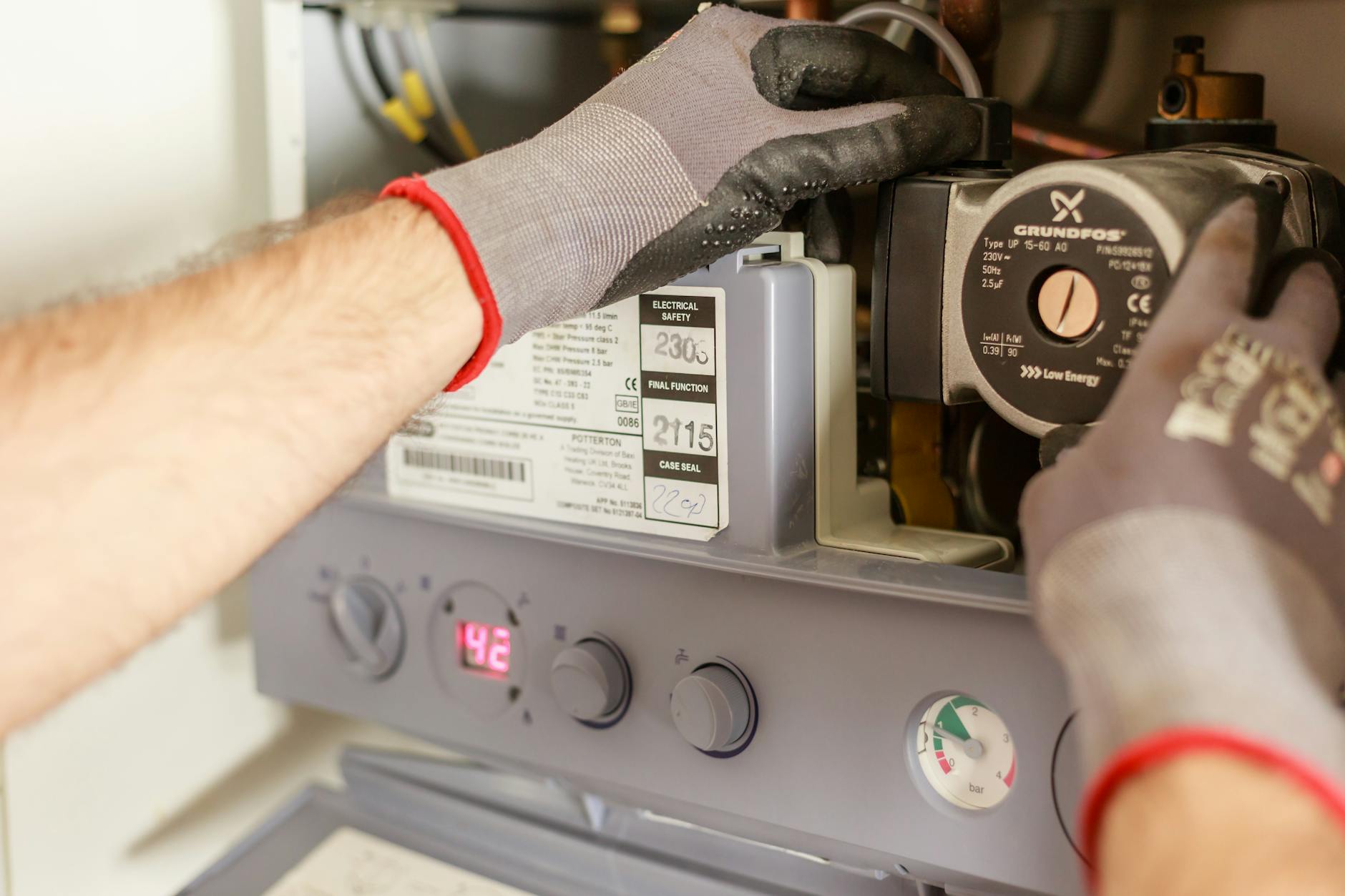

Home emergency insurance covers the cost of calling out a qualified tradesperson to deal with an emergency that makes your home uninhabitable or unsafe. Standard covers include: boiler and central heating failure in cold weather; total loss of electricity supply; burst pipes causing active water damage; blocked or broken drains causing sewage backup; failed main door or window locks creating a security risk; and roof damage allowing water ingress after a storm. The policy pays call-out fees and labour up to a defined per-event limit, with a standard excess per call-out.

Boiler Age and Condition Conditions

Boiler breakdown cover within home emergency policies is often subject to boiler age and condition requirements. Many policies restrict cover to boilers under 7, 10, or 15 years old. Some require the boiler to have been serviced annually by a Gas Safe registered engineer and may ask for evidence of recent service. Old, poorly maintained boilers are the highest risk for breakdown and some insurers simply exclude them from emergency cover.

How It Differs from a Boiler Service Plan

Home emergency insurance pays for emergency repairs when something breaks down unexpectedly. A boiler service plan - typically sold by energy suppliers and boiler manufacturers - includes an annual service and maintenance visits alongside breakdown cover. The service plan is preventive maintenance combined with breakdown protection; home emergency insurance is purely reactive. Many homeowners hold both - a service plan for maintenance and home emergency cover for other emergency scenarios beyond the boiler.

Limits and Exclusions

Home emergency policies set a maximum payable per event (typically £500-1,500) and a maximum number of call-outs per year. They do not cover: general maintenance; gradual deterioration; pre-existing faults known before the policy started; appliances beyond the policy definition of covered systems; and cosmetic repairs. The emergency must be sudden and unexpected to be covered.

Related Guides

Disclaimer

This guide is for general information only and does not constitute financial or insurance advice. Kaeltripton.com is not regulated by the FCA. Always read policy documents in full before purchasing cover.

Frequently Asked Questions

Does home emergency cover include boiler replacement?

No. Home emergency insurance covers repair of a failed boiler, not replacement if repair is uneconomical. If the engineer determines that the boiler is beyond repair, the policy typically pays up to the per-event limit toward the repair but does not fund a full replacement. New boiler costs - typically £1,500-4,000 installed - are not covered by emergency insurance. A boiler replacement is a capital expenditure, not an insured emergency repair.

Is home emergency cover worth having?

For homeowners without the savings to absorb a sudden emergency repair bill, home emergency cover provides financial certainty. The average cost per claim (call-out fee plus parts) for boiler repairs typically exceeds the annual premium. For newer properties with modern systems in good condition, the risk of emergency claims is lower and the value calculus differs. Consider the age and condition of your boiler and other covered systems when deciding.

|

★ Featured Partner · Sponsored Compare Insurance Quotes Search and compare quotes from leading UK insurers. Quotezone's panel includes specialist insurers not always on the four major comparison sites. Compare Quotes → |